Have you ever wondered what an overdraft facility is or how to apply for one? Learn more about it below and find out whether an overdraft facility is suitable for your needs.

An overdraft facility is a type of demand loan (a loan that the lender may require to be repaid at any time) which is offered by banks to enable a person to withdraw more money than they have in their account, based on a credit limit determined by the bank. This facility is also commonly known as a cash line facility.

The total overdraft amount is usually decided by banks, based on what you pledge as collateral to the bank. So if you were to pledge a property worth RM500,000 you would be able to get up to 50% of what you pledge, which in this case would be RM250,000. But the calculation method for an overdraft limit is based upon the bank’s discretion.

The asset you pledge as collateral to banks for overdraft can come in various forms. Depending on the bank, it could be in the form of unit trust, shares and bonds, property and even fixed deposits. Banks which offer overdraft facility in Malaysia are:

- Maybank Cash Line Facility (Overdraft)

- HSBC Personal Overdraft

- CIMB Credit Line Secured Overdraft

Take note that in order to apply for an overdraft; you must first have a bank account which actually offers the overdraft facility. However if your existing account does not offer an overdraft facility, you can still ask your bank on how you could make a request for one.

Are There Islamic Overdraft Facilities in Malaysia?

Yes, aside from being able to get an overdraft from conventional banks, there are also shariah compliant overdraft facilities available for Muslims and for those who prefer Islamic banking facilities. The overdraft facility from Islamic banks are made available either through the principles of Murabahah (sale on cost margin basis of cost plus), Bai Bithamin Ajil (deferred payment sale) or Bai Al Inah (sale and buy-back) principle. Example of an Islamic overdraft available in Malaysia is the Maybank Murabahah OD.

What Are The Advantages of An Overdraft?

What Are The Advantages of An Overdraft?

Flexibility

An overdraft provides you the freedom to decide how and when you make repayments as there are no fixed repayment schedules you need to adhere to. You decide when you want to settle both the interest and principal amount. So you can work out a payment schedule that works best for you.

Only Pay Interest For What You Use

You will only be charged interest on the amount that you actually use from the overdraft and not the total amount overdraft limit that you are granted by the bank.

What Are The Disadvantages Of An Overdraft?

Higher Interest Rates

Although an overdraft facility allows for flexible payments, you will be charged higher interest rates for this facility. You won’t be tied down to any fixed repayment schedule, giving you the freedom to decide when and how much you would like to pay.

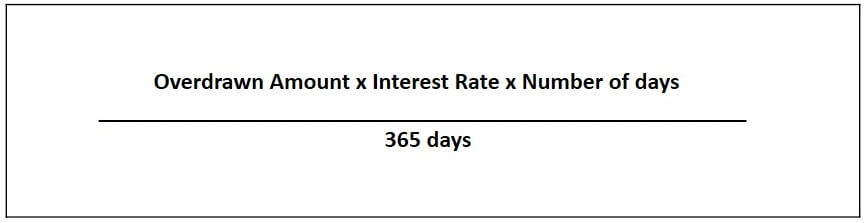

Interest will be charged on a daily basis based upon the amount of overdraft that you have utilised. The calculation of interest for an overdraft will reference against the Base Rate (BR).So the interest for an overdraft will be BR + interest rate. You can get a list of Base Rates for financial institutions here.

Formula to calculate the interest rate for an overdraft is as follows

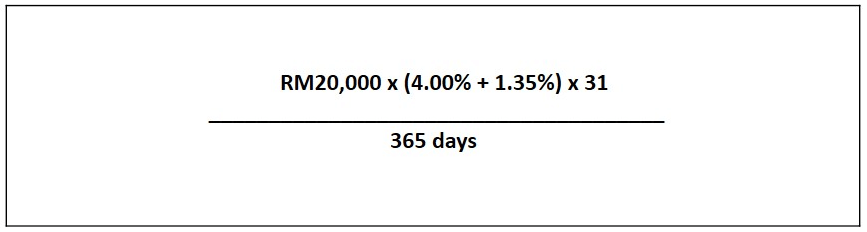

For example:

For example:

Overdraft amount used = RM20,000

Number of days overdrawn = 31 days of January 2016

Interest rate = BR (assume it is 4.0%) + 1.35% per annum

So the interest charged for January 2016 would be

Commitment Fee

Commitment Fee

A commitment fee is a fee that is charged by banks to you for the unutilised amount of your overdraft. And it is very important that you understand that the commitment fee is charged on the undisbursed amount, while interest is charged on the disbursed amount that has been utilised.

For example, if you have an overdraft limit of RM300,000, but have only used RM250,000. Interest will then be charged on the RM250,000 and a 1% per annum commitment fee will also be charged on the remaining RM50,000 portion of your overdraft limit which you did not use.

Requires Discipline

While the flexibility of an overdraft is a great advantage, it could also be the downside to this facility. If you don’t have enough discipline to make sure that you pay it through, an overdraft can become a long-term financial burden on you. If you are not disciplined with your payments, you may end up losing the asset you pledged on top of being charged hefty interest!

Unstable Credit Line

The bank can withdraw the overdraft facility at any time, so make sure you don’t rely too much on it. Aside from withdrawing the facility, banks can also revise or change the limit of your overdraft. Because of this, you should always think twice on choosing an overdraft and explore other financing options first.

Should You Use An Overdraft Facility?

Overdraft should ideally be used as a short term funding option, and when an emergency situation arises. You should not use an overdraft facility to finance your spending! One should also remember that an overdraft is really another form of loan, so it should not be treated as “extra cash” you have in your bank account to use whenever you fancy. An overdraft facility can be a good option when used wisely, but it can be a liability if you’re not smart about it, so proceed with caution!

See also: How Does a Balance Transfer Work?

Back to Blog

Back to Blog

.png?width=280&name=Tips%20To%20Choose%20The%20Right%20Banking%20Account%20CIMB%20(2).png)