[no_toc]

Do you know the differences between Islamic Finance and Conventional Finance? Some would probably simply say that Islamic Financing disallows interest-based transactions. Sounds easy to understand, right? But if interest rates are prohibited, then how does anyone gain from the initial investment. We'll cover the main differentiating factors between these two types of financing right here.

Before we move further, let's take a brief history lesson about Islamic Finance in Malaysia. The Islamic financial system in Malaysia has witnessed a tremendous growth in demand, acceptance and development since its introduction in 1963. It began with the establishment of the Malaysian Pilgrims Fund Board (Tabung Haji) and the country’s first Islamic bank, Bank Islam Malaysia Berhad (BIMB), which began operations on 1 July 1983.

Related: The Best Islamic Personal Loans in Malaysia

The Malaysian Islamic finance model is now one of the most advanced Islamic banking systems in the world. The goal of the Malaysian Islamic financial model is to operate in parallel with Malaysia's conventional financial system. To achieve this, the Islamic financial system presents itself as a viable alternative to the more established, conventional system.

What these two concepts really are?

Islamic personal financing has to be structured differently. This is because Islamic financial institutions are prohibited from making money through interest rates by lending money, There are various concepts, but most of them include the buying and selling of approved commodities and services following Islamic principles to make it Shariah-compliant.

Islamic personal financing is structured with profit rates, over the conventional interest rate. This is because the Islamic loan is not set up the same way a personal loan is.

An Islamic finance that works under the principles of Mudarabah is a form of business relationship: you provide the money, and the bank does business with it. As part of this relationship, a profit sharing ratio (PSR) is stipulated. Simply put, ( 95% of profits go to the bank, and 5% of the profits go to you).

Unlike interest, which is promised in advance by the bank regardless of how much profit the bank earns. The profits you earned (according to the PSR) are divided by the original amount you invested, which shows the percentage of profit.

Related: A Guide on Islamic Personal Loans

What's the difference between the two types of financing?

Conventional Financing Principles

In Conventional Financing, lenders lend to borrowers to make a profit from the interest charged on the principal amount. For property loans, borrowers pay an interest on the outstanding principal amount. Interest rates can be a fixed rate or based on a floating rate (e.g. Base Interest Rate (BLR),Kuala Lumpur Interbank Offer Rate (KLIBOR).

The loan contract for Conventional Financing is known as a Loan Facility Agreement. Payment is made over a set tenure by installments. A portion of each installment paid goes towards servicing the interest, while the remainder goes towards paying down the principal. The sooner the borrower can pay down the principal, the cheaper the amount of interest paid.

Islamic Financing Principles

Islamic Financing avoids interest-based transactions (Riba), and instead introduces the concept of buying something on the borrower’s behalf, and selling it back to the borrower at profit. In place of interest, a profit rate is defined in the contract. Like Conventional Financing, profit rates can be a fixed rate, or based on a floating rate (Base Financing Rate or (BFR).

Riba is a concept in Islam that refers broadly to the concept of, growth, increasing or exceeding. It has also been roughly translated as illegal, exploitative gains made in business or trade, under Islamic law.

Related: All You Need To Know About Loan Interest Rates

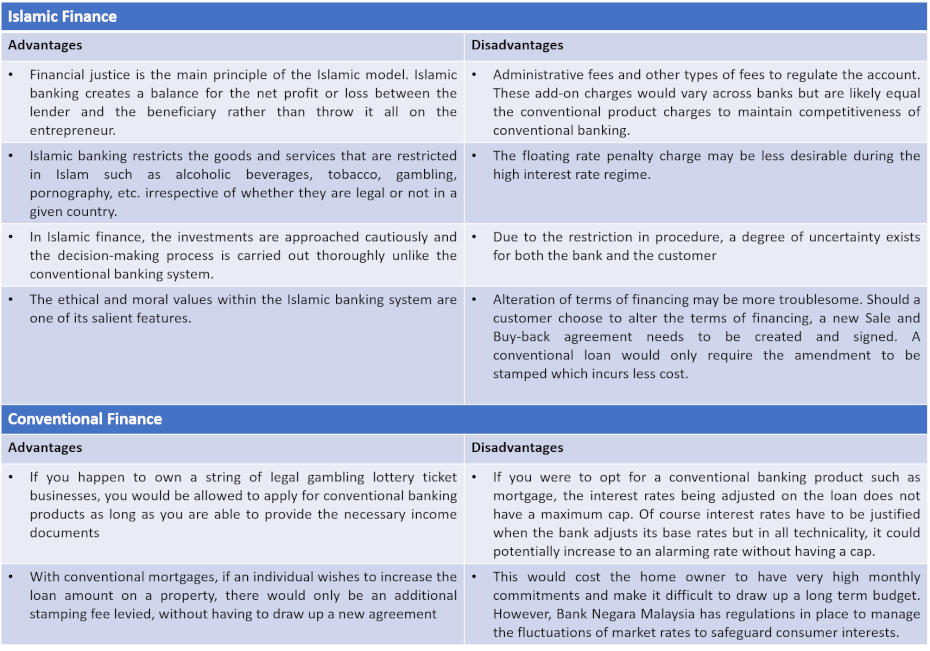

Pros and cons between both types of financing

Here's a short clip to understand Islamic Finance in under 2 minutes.

(Video courtesy of Al Rayan Bank YouTube channel)

Back to Blog

Back to Blog