Best Credit Cards in Malaysia

Compare Credit Cards from Malaysia's Top Banks

- View More Information

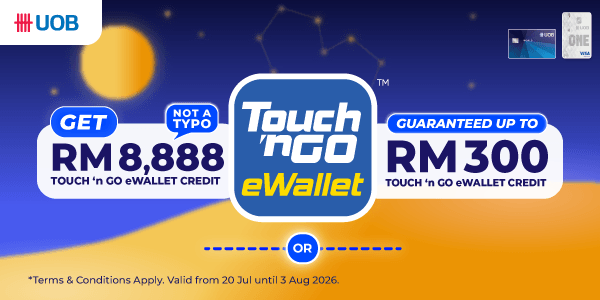

10% Cashback on Petrol & Dining

10% Cashback on Petrol & DiningUOB ONE Card

UOB ONE Card

- Min. Monthly Income

- RM 3,000 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free *

- Rewards Rate

- N/A

Simple high cashback with the UOB ONE Card

- View More Information

First year free!

First year free!HSBC Visa Signature Credit Card

HSBC Visa Signature Credit Card

- Min. Monthly Income

- RM 8,500 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free *

- Rewards Rate

- N/A

Earn up to 8x reward points on overseas and online spend, plus 6x Plaza Premium Lounge access at KLIA, Hong Kong, and Singapore Changi.

- View More Information

10x OCBC$ on weekends

10x OCBC$ on weekendsOCBC 365 MasterCard

OCBC 365 MasterCard

- Min. Monthly Income

- RM 4,000 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free *

- Rewards Rate

- N/A

Earns 10x OCBC$ on weekend shopping, dining and grocery spend.

- View More Information

Up to 10% cashback

Up to 10% cashbackAmBank Cash Rebate Visa Platinum

AmBank Cash Rebate Visa Platinum

- Min. Monthly Income

- RM 2,000 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free

- Rewards Rate

- N/A

A no-annual-fee cashback card that rewards your everyday spending. Earn up to 10% back on groceries, dining, transport, and online purchases.

- View More Information

5X Bonus Points on Everyday Spend

5X Bonus Points on Everyday SpendAlliance Bank Visa Platinum

Alliance Bank Visa Platinum

- Min. Monthly Income

- RM 2,000 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free *

- Rewards Rate

- N/A

Earn 5X Bonus Points on everyday spending with the Alliance Bank Visa Platinum

- View More Information

No Annual Fee!

No Annual Fee!UOB Simple Card

UOB Simple Card

- Min. Monthly Income

- RM 2,000 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free

- Rewards Rate

- N/A

Free for life with no annual fee, plus uncapped 10% cashback on finance charges.

- View More Information

Earn up to 5% cashback!

Earn up to 5% cashback!HSBC Live+ Credit Card

HSBC Live+ Credit Card

- Min. Monthly Income

- RM 8,500 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free *

- Rewards Rate

- N/A

Earn up to 5% cashback on dining, shopping, and entertainment, plus enjoy up to 15% off dining at 200+ restaurants across Asia.

- View More Information

Two cards, low-income entry

Two cards, low-income entryMaybank 2 Gold Cards

Maybank 2 Gold Cards

- Min. Monthly Income

- RM 2,500 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free

- Rewards Rate

- N/A

Two cards in one, with 5% cashback on weekends, 5x TreatsPoints on weekdays, including petrol spending. Enjoy zero annual fees for life!

- View More Information

Up to 12% Cashback at Shell

Up to 12% Cashback at ShellRHB Shell Visa Credit Card

RHB Shell Visa Credit Card

- Min. Monthly Income

- RM 2,000 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free *

- Rewards Rate

- N/A

Big fuel savings with the RHB Shell Visa Credit Card

- View More Information

10% Cashback on Online Spend

10% Cashback on Online SpendUOB EVOL Card

UOB EVOL Card

- Min. Monthly Income

- RM 3,000 / month

- Interest Rate

- 15% p.a.

- Annual Fee

- free *

- Rewards Rate

- N/A

Cashback for digital spenders with the UOB EVOL Card

More Information

Finding the best credit cards in Malaysia at CompareHero

At CompareHero, we know how much you value your time and money. That’s why we’re helping you save time by letting you pick a credit card with the best features all on one page.

No need to go to different bank websites because all the important information you need is right here. You’ll find popular credit cards from the top banks here in Malaysia. You could also find credit cards from the biggest and most trusted card networks, such as Visa and Mastercard.

We understand that credit cards are more than just a payment mode. If you use them responsibly, they’re a way to help you save money too.

That’s why our top credit card picks come with the highest earning rates and unique offers you won’t find anywhere else.

How do the CompareHero best deals work?

All of the credit cards you see here are there for a reason. These are the ones chosen by many of CompareHero’s users for their exceptional rewards and features.

With so many cards competing for your attention, you’re getting help from others to narrow down your search for the perfect one to suit your lifestyle.

So whether you’re looking for a credit card that gives you the best cashback rates, the most reward points or one that lets you earn air miles fast, start your search here at CompareHero! We’ll show you which credit cards offer the most cashback at your favourite supermarket or which air miles cards have the highest earning rate for local spending.

Narrow down your choices by choosing your top three and comparing their features.

How to find the best credit card to suit your needs and lifestyle?

View your choices above to find one with the features you need. For example, if you're looking for a credit card that gives you reward points for every Ringgit spent, search for a card that offers the highest earning rate.

Or if you're an avid traveller, choose a card that offers free airport lounge access and cashback on overseas spending, for instance. Once you have a card in mind, simply click on the “Apply Now” button on the card of your choice to begin the fast and easy application process online.

The typical requirements or documents that you need to be ready with include:

• A copy of your MyKad/IC

• Your latest salary slips/commission statement

• Your latest EPF statement

You’ll also have to meet certain income requirements, and this differs depending on the card you apply for.

Compare the Best Credit Cards in Malaysia

What are the benefits of comparing credit cards?

Comparing credit cards will help you find a card to suit your spending needs and lifestyle. You will be able to narrow down all the best credit cards with the most benefits and rewards for every Ringgit you spend. This includes earning air miles for every local and overseas spend, earning cashback on categories like Dining, Online Shopping, and Petrol, to name a few, and earning rewards and discounts for every spending you make. If you apply through our comparison website, you'll also stand a chance to get exciting credit card sign-up offers!

How does the comparison tool work?

We do the hard work for you by consolidating all the credit cards available in the market into a single site, here at CompareHero. Just fill in the requirement information, and you'll find all the cards that suit your requirements within a matter of seconds. Review the various details available and select a credit card that suits your lifestyle needs. The cards included in our comparison tool are based on the most trusted financial institutions in Malaysia. We have included a wide range of banking industry leaders who can give you the best credit card options.

What is a credit card?

A credit card is an alternative payment method for goods and services. It is essentially a type of short-term loan that is issued by a bank or financial institution; this is where the term “credit card” comes from. With a credit card – in simple terms – the bank lends you money first and then you repay it in credit when it is due.

What are the different categories of credit cards?

• Best Deals Credit Cards: Our most popular credit cards for their exceptional rewards and features, be it the best cashback rates, the most reward points or one that lets you earn air miles blazingly fast, start your search here!

• Best Cashback Credit Cards: Cashback credit cards convert every Ringgit that you spend into attractive cash rebates. The amount of rebate you get depends on the cashback rate of the particular credit card.

• Best Air Miles Credit Cards: This type of credit card is designed to allow you to earn air miles every time you spend on selected categories. These cards give you access to a loyalty program offered by prominent airlines.

• Best Rewards Credit Cards: Rewards credit cards allow you to collect and accumulate rewards points that can be traded for a range of benefits, such as vouchers and discounts.

• Best No Annual Fee Credit Cards: No annual fee credit cards are exempt from being charged your usual annual fee. However, be sure to read the fine print to see how long the offer is valid and if there are any terms to this. A no-annual-fee credit card will result in savings as you are not required to pay this fee.

• Best Islamic Credit Cards: An Islamic credit card is Shariah compliant, with the prohibition of gharar (overcharging) and riba (interest). Islamic credit card often offers takaful coverage. Aside from that, Muslims will also have the added convenience of being able to pay their Zakat with an Islamic credit card.

What is a supplementary credit card?

It is an additional card that is issued under a principal account holder’s name. Basically, it is a secondary card that works under the same main account, making it easy to consolidate all payments under a single account, and you can also earn rewards at a faster rate. A supplementary card is usually given to a family member for emergencies and the cardholder does not need to fulfil any requirements aside from being at least 18 years old to be eligible.

When is the best time to use a credit card?

As a credit card works similarly to having a short-term loan, it is ideal as a substitute for cash to spend on your daily goods or services, such as groceries or clothing. It is also ideal for slightly more expensive purchases such as a laptop or an expensive timepiece, as carrying a large amount of cash can be very dangerous.

There is a limit as to how much you can spend on a credit card, however. This limit is decided by the bank based on your credit history and monthly income and differs from person to person. Do keep in mind that you must pay the credit card by the outstanding due dates or you will be charged interest. A credit card is not a good solution for long-term financing because of its high interest rates. In fact, it can be one of the more expensive options as some credit cards charge an interest rate of 18% per annum, the highest in the market.

Instead, a personal loan would be a better option for long-term financing with interest from as low as 4.99% per annum. Credit card interest rates differ between banks and types of credit cards. It may fluctuate based on your repayments too; if you pay promptly, you’ll be rewarded with a lower interest rate.

Your credit score can also impact the interest rate offered to you. Typically, the healthier your credit score, the lower the interest rate. In Malaysia, you can obtain a copy of your credit report from CCRIS or CTOS.

What is a credit limit?

A credit limit is the maximum spending limit that is applied to your credit card when you apply for one. The credit limit is determined by two factors: your credit history and your monthly income. In Malaysia, cardholders earning RM36,000 or less per year have a credit limit that doesn’t exceed two times their monthly salary; those earning RM36,000 and above have their credit limit determined at the bank’s discretion.

What is the difference between a credit card and a debit card?

The main difference between a credit card and a debit card is where the money comes from when making a payment or purchase.

• Credit Card

• Allows you to spend borrowed money and repay it later

• Has a credit limit

• Isn’t linked to your bank account

• Allows for instalment payments

• Debit Card

• Directly linked to your bank account (current or savings)

• You can only spend money you have in your account

• Money spent is directly deducted from your bank account

Why do I need a credit card?

While a credit card can pile on your debts, it is a very useful tool that can bring a lot of benefits through its features. You must be disciplined and keep in mind that you have to make repayments at the due date responsibly.

• Safer than cash

• Enjoy protection on some purchases such as flight insurance

• Enjoy benefits such as reward programmes and points, cashback and rebates, air miles, and exclusive discounts and promotions with retail transactions at selected outlets, restaurants, and services. Get more out of your retail spending!

• 0% interest instalment plans (over several months) for more expensive purchases, such as a computer or a smartphone

• Helps to build credit scores which is important when applying for other financial services such as a car loan

How does a Credit Card work?

When you purchase with a credit card, be it through an online portal or swipe at the payment terminal in a brick-and-mortar shop, the payment process goes through a process with several parties in the back. It will be a simple and near-instantaneous experience for you, however. Typically, there are five parties involved in a credit card transaction:

• Cardholder: You or any other authorised person (like your spouse or children to whom you’ve given supplementary cards) can use the credit card to make purchases.

• Card Issuer: Institutions, such as banks and consumer finance companies, that issue credit cards.

• Credit Card Network: Organisations that set up the payment ecosystem and act as the middlemen between merchant acquirers and card issuers (like Visa, Mastercard and American Express, for example).

• Merchant Acquirer: Institutions, often banks, process credit card transactions for merchants using a POS terminal.

• Merchant: Retailers, restaurants and e-commerce sites around the world allow credit cards as a form of payment.

The Pros and Cons of a Credit Card

Like many things in the world, the credit card is not without its ups and downs. It is very important that you understand the pros and cons of a credit card. When managed correctly, the credit card brings a lot of benefits and rewards, but if mismanaged, the credit card can be an instrument that leads to high debt.

• The Advantages

• Speed and Efficiency: A credit card is extremely easy to carry around and paying with one is quick and seamless, often requiring nothing more than a swipe or tap on the payment terminal.

• Protection: Credit card providers usually offer their customers protection on purchases made with their cards. A purchase protection plan typically offers coverage against theft or accidental damage. Coverage varies between providers.

• Buy Now, Pay Later: For times when you need to make an expensive purchase and can’t afford to pay for all of it in one go or during those really limited sale periods, credit cards are a great solution.

• Instalment Plans: With features such as the Easy Payment Plan (EPP), you can break down your expensive purchases into monthly repayments with 0% interest (varies among providers). If you miss the payment deadline, then you’ll have to pay either a penalty fee or have the full interest added to your outstanding balance at the end of every month.

• Earn Benefits while You Spend: Making purchases with a credit card can allow you to rake in rewards such as cashback, reward points, and air miles.

• Emergency Cash: If, for some reason, you are unable to withdraw cash from the ATM or your debit card isn’t working, a credit card can be used for advance withdrawals.

• Good for your Credit Score: Responsibly using a credit card can help build your healthy credit score, which is then used to determine your application eligibility for other financial products and services.

• The Disadvantages

• The Debt Trap: It’s all fun when you’re swiping and tapping your credit card everywhere and it’s easy to forget you’re spending borrowed money. It’s especially easier to forget because you’re not parting from physical cash. Keep track of how much you’re using your credit card so you don’t build up an outstanding you can’t pay.

• Hidden Charges and Fees: A credit card may come with other “hidden” charges and fees such as an annual fee, late-payment fee, and even penalty fees for exceeding your credit limit.

• Expensive cash advance: Cash advancement on a credit card is often for an emergency and should be treated as one. The interest rate for advance cash withdrawals is high, between 17-18% and you can get charged a transaction fee.

• Can be bad for your credit score: It is only bad if you are unable to manage your credit card repayments responsibly, such as missing out on payments or not paying the full amount due.

• Fraud and Scams: A credit card is susceptible to fraud and scams, even with safety and security features to protect your account and the card. It is very important that you do not simply divulge your credit card information to anyone.

Credit Card Charges and Fees

A credit card has several different types of fees and charges. Some of these depend on what you use the credit card for and some may be just a general fee. Here are some of the most common fees and charges.

Annual Fee

This is a type of fee that is charged yearly for the privilege of owning a credit card. Not all credit cards have an annual fee, however. Some cards may also waive the fee depending on how much you spend.

Cash Advance Fee

The interest rate charged for a cash advance withdrawal can go up to 18% per annum; there is a one-time transaction fee for the cash withdrawal too.

International ATM Withdrawal Fee

You will be charged a one-time transaction fee as well as the bank’s currency rates – typically higher than the usual.

Balance Transfer Fee

When transferring balances to another credit card, you will be charged 0% to 5% per annum on the total amount as transfer fees.

Late Payment Fee

A fee is charged when you miss out on a monthly repayment; this fee is either a flat rate or a percentage of the total repayment, whichever is higher.

What are credit card interest rates and how is it calculated?

Interest is a charge applied by banks for lending you money. It is calculated as a percentage of your outstanding balance. The rate is determined by the bank upon review of your credit history and other factors in your application; it is usually between 15% to 18% per annum. The better your credit score, the lower your interest rate. A healthy credit score demonstrates that you are in a healthy financial position and it is less risky for the bank to approve your application, therefore charging you a lower interest rate.

Applying for a Credit Card

How do I apply for a credit card in Malaysia?

Research!

It is very important to understand what you want a credit card for. There are many different credit cards out there that have different benefits and features that may fit different lifestyles. You can use a credit card comparison tool like our very own to help you out. Just fill in the required details and the tool can automatically draw up the suggested credit cards for your needs. Make sure you read all the little details about the card such as the charges, benefits, interest rates, and most importantly if you meet the minimum requirements.

Check your Credit Score

Your credit score is what banks will mostly use to determine if you can get a card. There are various credit scoring agencies that can provide you with a credit scoring report such as CTOS and CCRIS. If you have a healthy credit score, then you should be easily approved for a credit card.

Understand you may not get the rates advertised online

The rates you see online may not necessarily be the rates you’ll receive when you apply for a credit card. This is because the bank determines the final rates of everything based on each individual’s financial profile.

Apply online or at a bank branch

Once you’ve determined the right credit card to get, you can either apply online on our website or in person at a bank branch. An online application is generally much faster and more convenient. If you are applying online on our website, you will need to fill in the form after you click on “Apply Now”.

If you are walking into a bank branch, you will need to provide several documents, such as:

• A copy of your MyKad/IC

• Your latest 3 months salary slips/commission statement

• Your latest 6 months' savings account activity statements

• Your latest EPF statement, etc.

What are the best credit cards should I get?

By now, you must be asking "What is the best credit card for me?". Therefore, here are some of our recommendations:

For Cashback

• Standard Chartered Simply Cash Credit Card

• UOB ONE Card

• AEON BiG Visa Gold

For Rewards

• UOB Lady's Card

• HSBC Visa Signature

• RHB Rewards Visa Credit Card

For Petrol

• RHB Shell Visa Credit Card

• Petronas Maybank Visa Gold

• Public Bank Petron Visa Gold

For Air Miles

• Singapore Airlines KrisFlyer American Express Platinum

• Public Bank World Mastercard Credit Card

• Standard Chartered Journey Credit Card