The Malaysian Employee Provident Fund (EPF) was established in 1951 as a compulsory savings plan for retirement, especially for employees in the private sector.

However, many decades later, our EPF contributions as a whole are not what they should be. Recent reports have shown that only 4% of Malaysians are able to retire comfortably, by EPF’s own calculations.

The reasons for this are many, including withdrawals made during the Covid-19 pandemic for emergency use and stagnant salaries among locals, resulting in insufficient contributions.

In addition to this having a negative effect on individuals, it also affects the economy as a whole. The nation will have to struggle with higher costs in sustaining retirees if a large majority have insufficient savings.

That’s why it’s useful to know about EPF’s voluntary contribution option, which many are still not aware of. This program offers more flexibility for Malaysians to manage their savings, and can be an option for propping up one’s retirement funds.

We’ll look into this program in detail later on. First, we should understand what the EPF is in Malaysia.

How Does the EPF Work in Malaysia?

The Employee’s Provident Fund was set up in 1951, with the passing of the Employee’s Provident Fund Ordinance 1951. It was meant to be a social security scheme to provide retirement benefits to its members for added financial security. In Malay, the EPF is known as Kumpulan Wang Simpanan

As of 2024, EPF Malaysia covers more than 15 millions members, managing contributions worth over RM800 billion.

When the EPF began, it started with mandatory contributions. Employees were required to contribute a portion of their gross income (currently 11%) and employers would top up an additional 12-13% of their employee’s salary.

If you’re employed, this will be handled by your administrative department. You’ll see this reflected in your payslip as a deduction of your gross salary.

The EPF manages all contributions like an investment fund. In simple terms, they invest our collective EPF contribution in various businesses, equity funds, properties and the like. This generates a profit, which is paid out yearly to members. It is usually announced as a percentage of your contributions, which varies from year to year.

Upon reaching the age of 55 and 60, members are allowed to withdraw their contributions lump sum plus the dividends earned. Withdrawals for other reasons, like education and property purchases are also allowed before you reach the stated age..

With the changing nature of employment and income generation in Malaysia, EPF has begun introducing voluntary contribution options as well.

How Does EPF Voluntary Contribution Work?

In addition to Mandatory Contributions made by both employers and employees, members are given several options to make voluntary contributions. These have been introduced to include those who are not in a conventional employment arrangement, are self-employed or simply want to add to their EPF savings.

There are currently four EPF Voluntary Contribution programs:

1. Self-Contribution

This self-contribution program is meant for those not covered under the EPF Act 1991. Basically, this includes those not employed under a conventional employee-employer arrangement. For instance, those who are self-employed, run their own business, or are freelancers.

This is also useful for remote workers whose employers are located overseas. In cases like these, foreign employers usually don’t make an EPF contribution in Malaysia for you, so you can consider this option and contribute on your own initiative.

Self-contribution can also be made by those who have previously been employed but now are working outside the mandatory contribution system.

Who can apply:

- Malaysian citizens and permanent residents

- Below 75 years old

- Registered EPF member

2. i-Saraan Scheme

The i-Saraan programme was made especially to encourage gig workers and those without fixed incomes to save for their retirement. It offers a lot of extra benefits including:

- Incentive of 15% of total contributions for the year up to RM500. Lifetime incentive limit of RM5,000 or until the member reaches 60 years of age, whichever is earlier.

- Tax reliefs

- Death benefits

The i-Saraan scheme is a little more special in that you’ll have to register for it on their website.

You can also register for it at any EPF branch office, Self-Service Terminal or using the KWSP i-akaun (more on how to start one later).

Who can apply?

- Malaysian citizens

- Below 60 years old

- Must be self-employed with no employer

- Registered EPF member

3.i-Suri Scheme

This scheme was designed to provide housewives and homemakers a way to save and grow their wealth for their old age. This way they will be able to save a portion of any income they make or allowance they receive from their spouse or any other family member.

In fact, there is a separate scheme called i-Sayang where husbands can contribute 2% of their salaries to their wife’s EPF account.

The i-Suri scheme offers added benefits to members:

- Incentive of 50% for every RM1 contributed, capped at RM300 for the current year. Incentive capped at RM3000 or until the member reached 55 years of age, whichever comes first.

- Tax relief

- Death benefits

- Malaysian citizens

- Below 55 years of age

- Registered EPF member

- Housewives registered under eKasih ( the National Poverty Data Bank)

4. Account-1 Top Up Savings

This voluntary contribution scheme allows EPF members to contribute to the EPF savings of their loved ones. This can be from children to parents, from one spouse to another, from parents to their children and so on.

The only condition is that the person contributing must be below 55 years and be a registered EPF member.

The recipient can be a member or non-member, and need to fill in this form in order to start receiving contributions from their loved one.

How Can I Start Voluntary Contributions?

If you are not yet an EPF member, you should register and open an account first. It’s pretty easy to do so these days. Once you already have an account (or if you’ve had one for years already), proceed to open an online account called an i-Akaun.

If you often ask ‘How do I check my EPF number in Malaysia?’ or ‘How do I check my EPF balance in Malaysia?’, then i-Akaun is your answer as it has all this information and more. It’s also the most convenient way to make voluntary contributions.

Method 1: Via i-Akaun

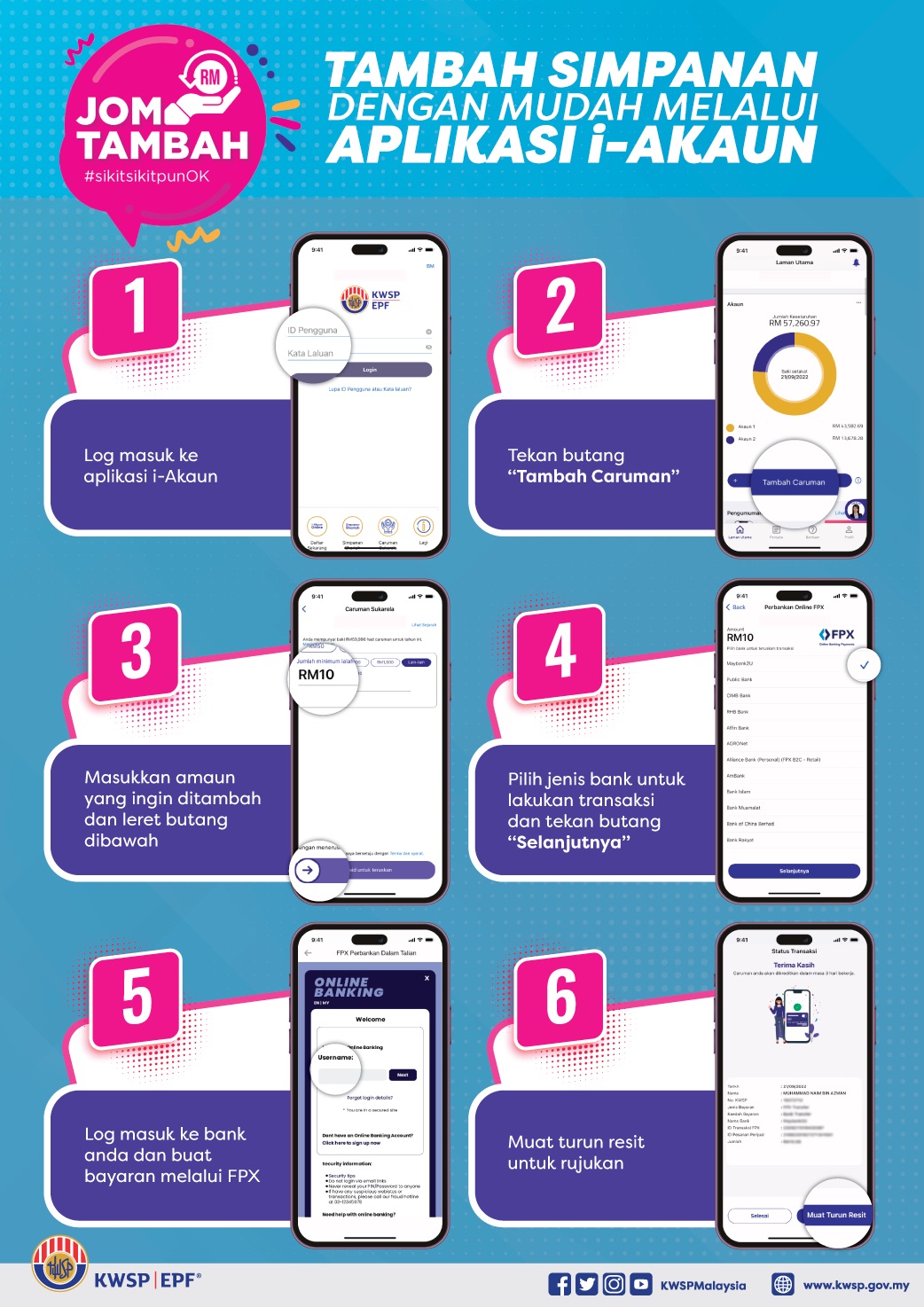

Even if you’re already an EPF member for years, you may not necessarily have an online EPF account known as an i-Akaun. Registering for one is easy and will allow you a lot of conveniences. Your i-Akaun can be started or accessed through their website as well as by downloading the i-Akaun app.

If you already have an i-Akaun, log in and select ‘Add Contribution’. Enter the amount you want to contribute, and slide the bar to proceed. There’s no minimum per transaction, but voluntary contributions must not exceed RM100,000 per year.

You’ll be guided through the FPX payment process. Basically it’s like making payments for e-commerce purchases, just like shopping online.Your deposit will be reflected in your account within 3 working days.

Method 2: Via Bank Transfers

Check whether your banking app has EPF as a payee, usually under the ‘Payments’ or ‘Bills’ section. You’ll be asked to fill in your details including your EPF number in Malaysia. The deposit will be made to your EPF account thereafter within 3 working days.

Method 3: Via Bank Agents

You can make electronic or cash payments to EPF’s bank agents, usually through the counter. You’ll have to fill in the self-contribution form form and submit them with your payments. There are four Bank Agents including Bank Simpanan Nasional (BSN), Maybank, Public Bank and RHB Bank.

Method 4: Via EPF Counters**

EPF offices nationwide also accept deposits for voluntary contributions. You can even deposit in cash, but this is capped at RM500. They also accept debit cards, cheques, bank drafts, money orders and postal orders. Just like with bank agents, you’ll have to fill in and include the self-contribution form with your deposit.

*Apart from these four methods, you can also look out for EPF mobile teams who can also receive voluntary contributions.

** Account-1 Top Up Savings program only receives deposits via EPF counters

Final Thoughts

The main question you may have now is, why should we invest in EPF for retirement? There are many other retirement schemes or insurance plans available. The reason is that EPF is a pretty stable and low risk investment, with acceptable returns every year.

In fact, the EPF rate in Malaysia for dividends is about 5-6% per annum, on par with the best low to medium risk investment funds.

Saving money on a monthly basis is your first step in building a healthy retirement fund. Check out some of the best cashback credit cards to help you achieve your savings goals. Compare the best credit cards for cashback with us to get even more savings!

Back to Blog

Back to Blog