Debt Management

Important guides on how to manage your debt.

All articles

5,272 Malaysians Under Age 34 Declared Bankrupt Since 2020

Last updated

Mar 13, 2025

4 Ways To Spring Clean Your Finances

Last updated

Dec 21, 2022

6 Ways To Pay Off Your Credit Card Debt

Last updated

Oct 5, 2022

What Is Lifestyle Inflation & Why It Could Make You Poor!

Last updated

Jul 15, 2022

What happens to our debts when we die?

Last updated

Jul 1, 2022

4 Ways To Keep Your Family Financially Protected After Your Death

Last updated

Jun 7, 2022

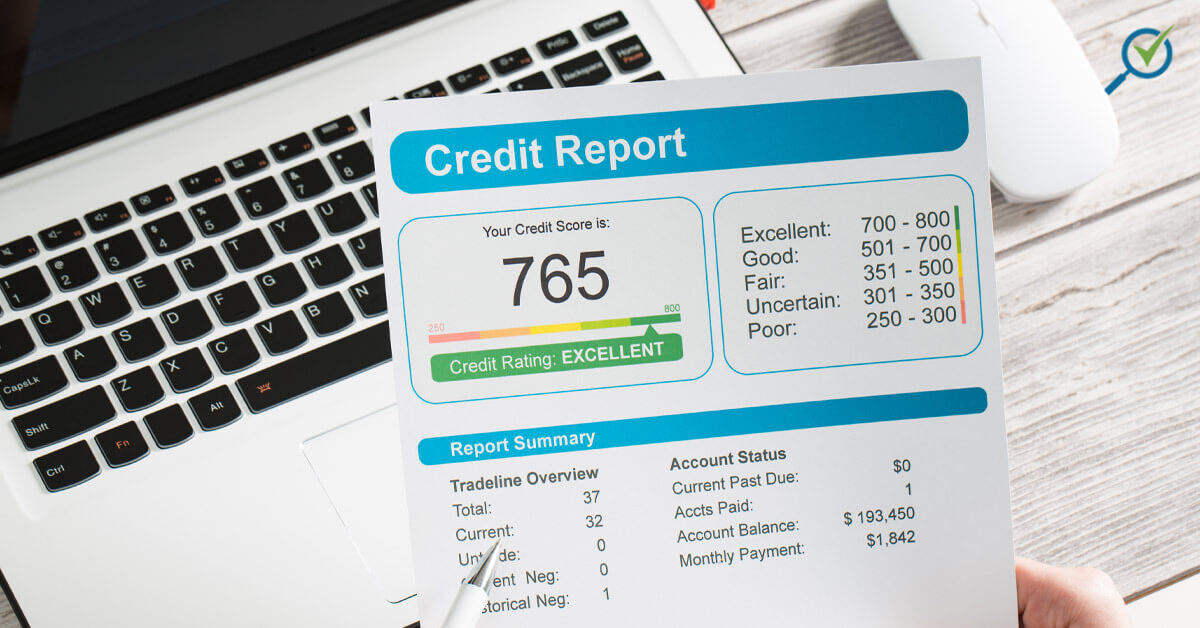

Ultimate Guide To Credit Scores

Last updated

Mar 8, 2022

How do I calculate my Debt Service Ratio?

Last updated

Dec 28, 2021

What Actually Happens When You Go To AKPK For Help?

Last updated

Dec 22, 2021

Apa Anda Perlu Tahu Tentang Status Muflis

Last updated

Dec 15, 2021

3 Ways You Can Settle Your Debts In Malaysia

Last updated

Sep 10, 2021

Perbezaan Antara Hutang Baik dan Hutang Buruk

Last updated

May 5, 2021

4 Cara Cepat Untuk Membayar Hutang Pinjaman Peribadi Bank

Last updated

May 4, 2021

7 Common Things Malaysians Don’t Realise Are A Waste Of Money

Last updated

Apr 28, 2021

Know The Difference Between Good Debt and Bad Debt

Last updated

Apr 28, 2021

6 Sebab Mengapa Hutang Along Memudaratkan Kehidupan Anda

Last updated

Apr 27, 2021

How Do You Survive From Bankruptcy?

Last updated

Apr 27, 2021

What To Do When Debt Collection Agency Knocks On Your Door

Last updated

Mar 9, 2021

What You Need To Know About Bankruptcy In Malaysia

Last updated

Feb 10, 2021

Apakah Perbezaan Antara Hutang Baik Dan Hutang Lapuk?

Last updated

Feb 2, 2021

Bagaimana Untuk Menghadapi Pengutip Hutang?

Last updated

Jan 26, 2021

Apakah Perbezaan Laporan Kredit CCRIS dan CTOS?

Last updated

Jan 25, 2021

Urus Hutang Anda Secara Percuma Bersama AKPK

Last updated

Jan 18, 2021

What Happens If You Can't Pay Your Loans In Malaysia Post-MCO (And How To Fix This Fast)

Last updated

Jul 1, 2020

7 Strategies To Get Out Of Debt Fast During The COVID-19 Pandemic

Last updated

Jun 4, 2020

Are You Financially Better Or Worse Than Average Malaysian? [INFOGRAPHIC]

Last updated

Sep 12, 2019

Money Management: 3 Ways to Control Your Finances

Last updated

Apr 19, 2019

Resolve Your Financial Complaints For Free With The Financial Mediation Bureau!

Last updated

Apr 3, 2019

Panduan Memilih Agensi Laporan Kredit yang Sesuai

Last updated

Mar 22, 2019

Pelan Pindahan Baki Terbaik di Malaysia

Last updated

Mar 22, 2019

Lakukan Langkah ini Jika Anda Tiada Skor Kredit

Last updated

Mar 22, 2019

Bagaimana Untuk Mengira Nisbah Khidmat Hutang Anda?

Last updated

Mar 21, 2019

MFPC Terangkan Sebab Rakyat Malaysia Muflis

Last updated

Mar 21, 2019

5 Ways to Avoid The Dangers Of Credit Card Debt

Last updated

Mar 21, 2019

Mengapa Rakyat Malaysia Mempunyai Hutang Kad Kredit?

Last updated

Mar 4, 2019

How To Deal With Gambling Addiction In Malaysia

Last updated

Mar 2, 2019

Our Mission

We'll help you make your next financial move the right one.