Personal Finance

Guides On How To Manage & Maximise Your Personal Finances

All articles

PSA: If Your Cat Pees on Your Passport, You Need to Fork Out RM400 to Replace it

Last updated

Aug 25, 2025

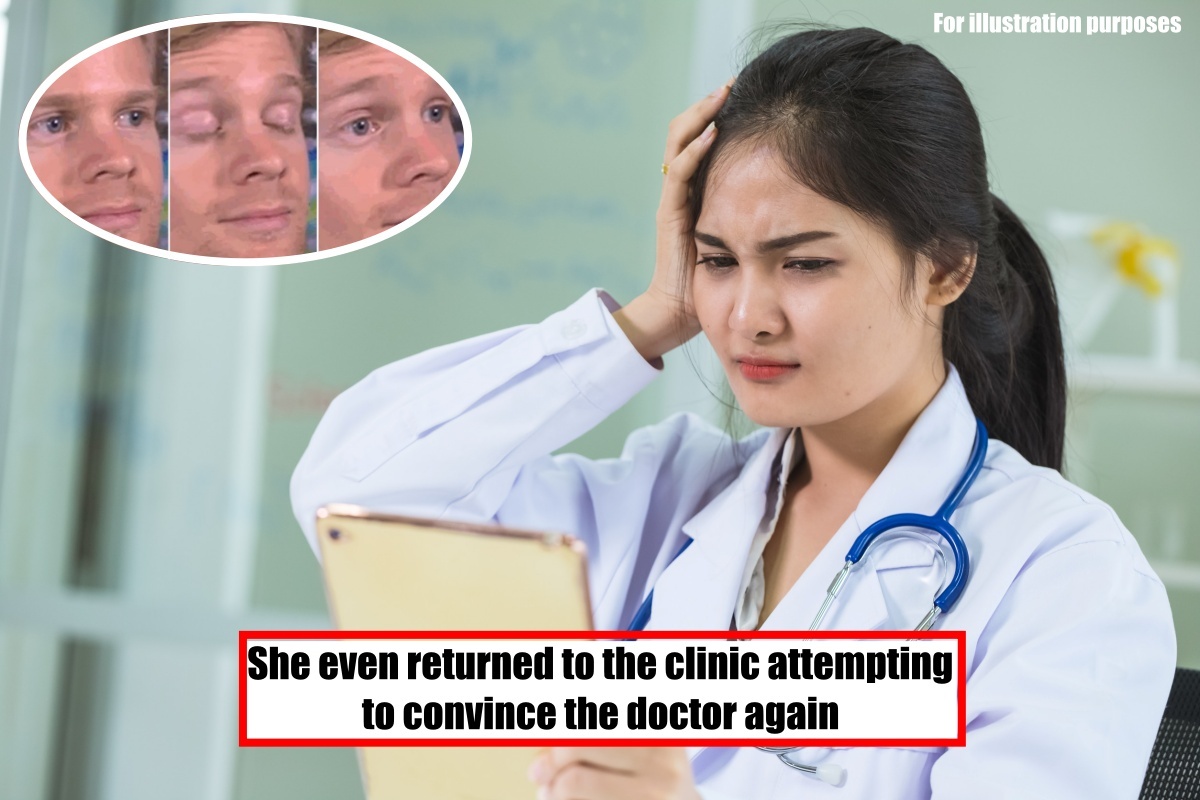

Doctor Exposes Patient Who Tried To Turn RM50 Medical Bill Into RM350 Claim, Twice!

Last updated

Aug 25, 2025

“Not wife material!” – Freeloader M’sian Yells at GF in Public for Not Paying for His Meal

Last updated

Aug 22, 2025

Woman Begs for Money, Later Spotted Enjoying Jollibee Date With Her BF

Last updated

Aug 22, 2025

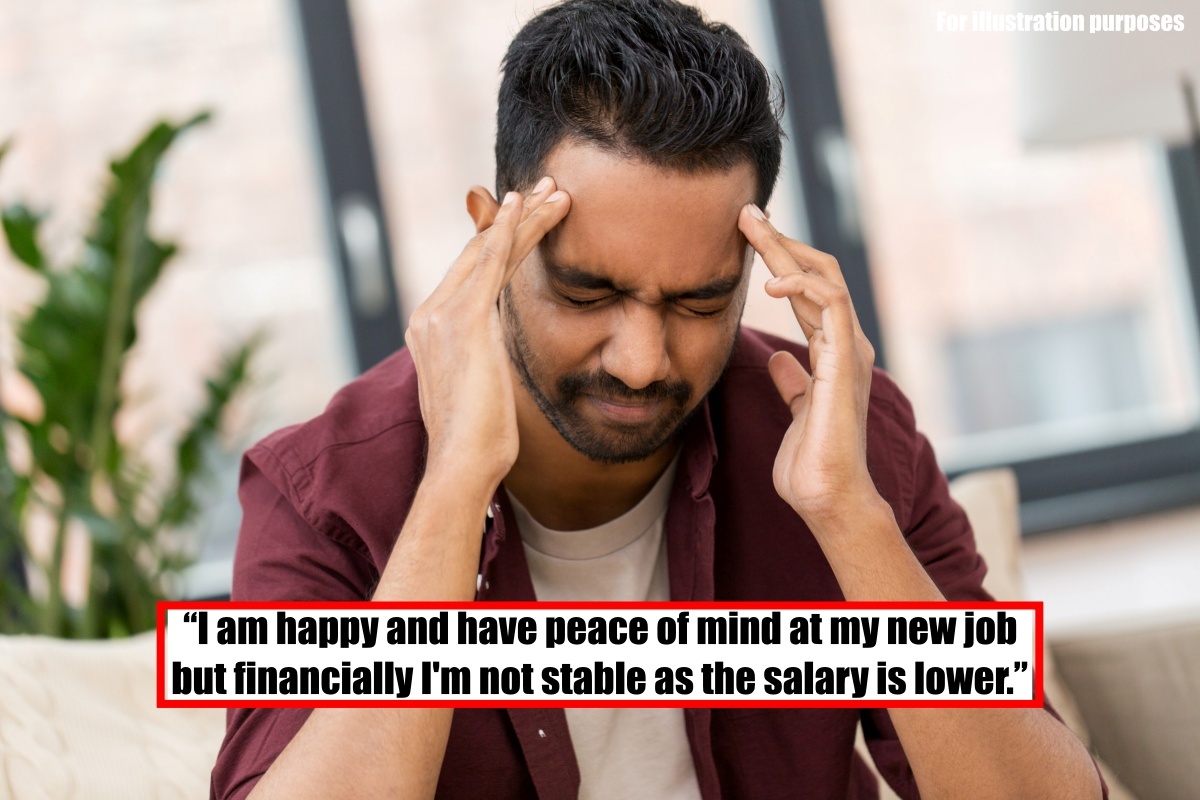

M’sian Quits Stressful RM4k Job for RM500 Pay Cut, Now Struggles With RM3.8k Bills

Last updated

Aug 22, 2025

M’sian Shares Secret Behind Winning 6 Cars, 10 Bikes, JLo VIP Concert Tickets and More!

Last updated

Aug 22, 2025

RM800k in a Backpack! SG Woman’s Jackpot Win Turns Into a Stressful Journey Home

Last updated

Aug 21, 2025

Influencer Buys Rare Yamaha RXZ for RM146,000, Sells it for RM1 Million a Year Later

Last updated

Aug 21, 2025

“I expected RM7k” – M’sian Shocked Fiance Managed to Save Only RM500 for Wedding

Last updated

Aug 21, 2025

Ex-Monk Sues Daughter for RM118k in Parental Support After Going Broke

Last updated

Aug 21, 2025

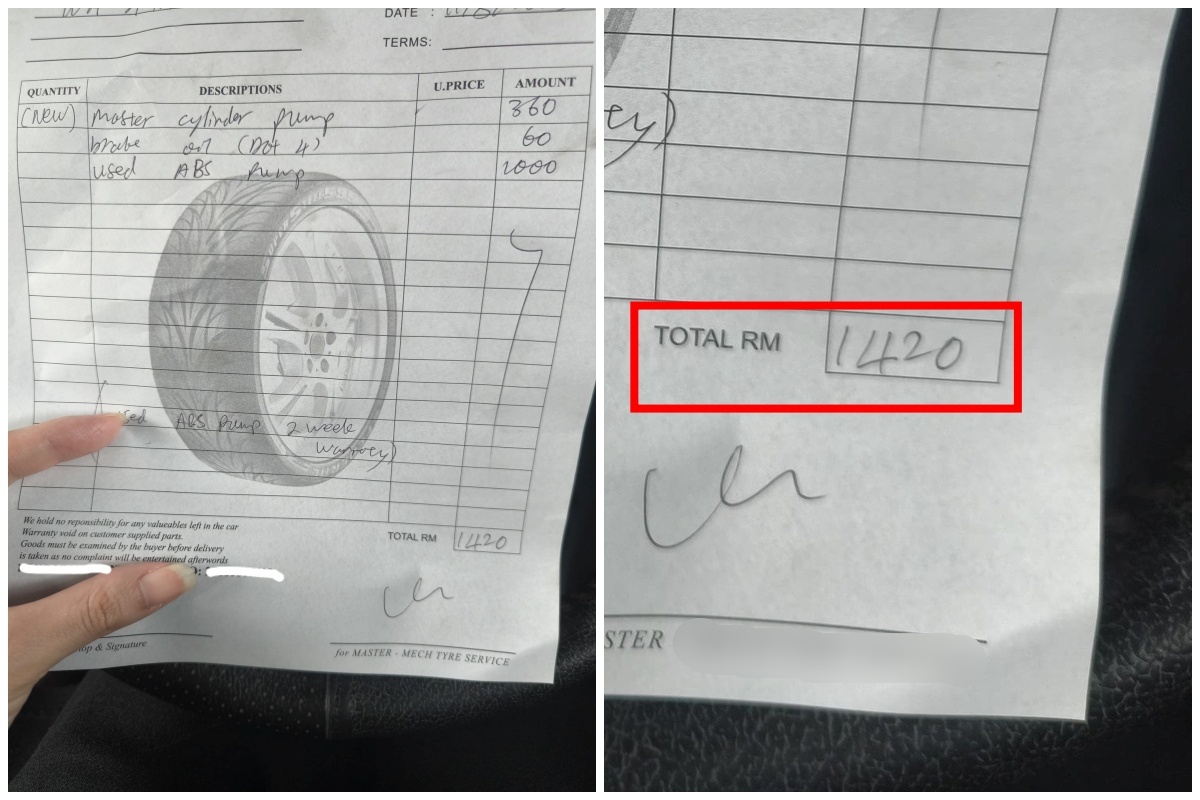

M’sian Woman Charged RM1,400 for Used ABS Pump for Her Perodua Axia

Last updated

Aug 20, 2025

M’sian Forced by Colleague to Fork Out RM300 for Office Crush’s Birthday

Last updated

Aug 20, 2025

“I was just his ATM” – M’sian Exposes Fiancé Who Cheated and Kicked Her Out

Last updated

Aug 20, 2025

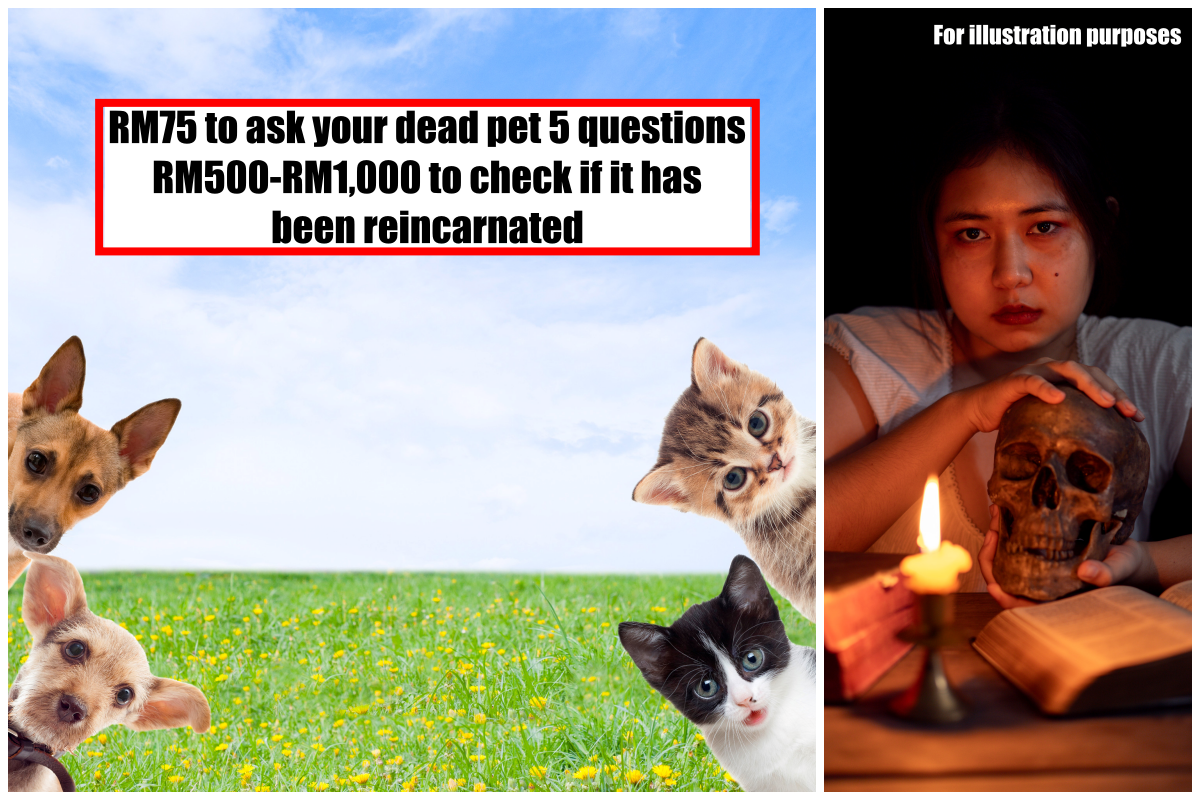

Owners Spend RM1k on Psychics to Talk to Dead Pets, Get Scammed Instead

Last updated

Aug 20, 2025

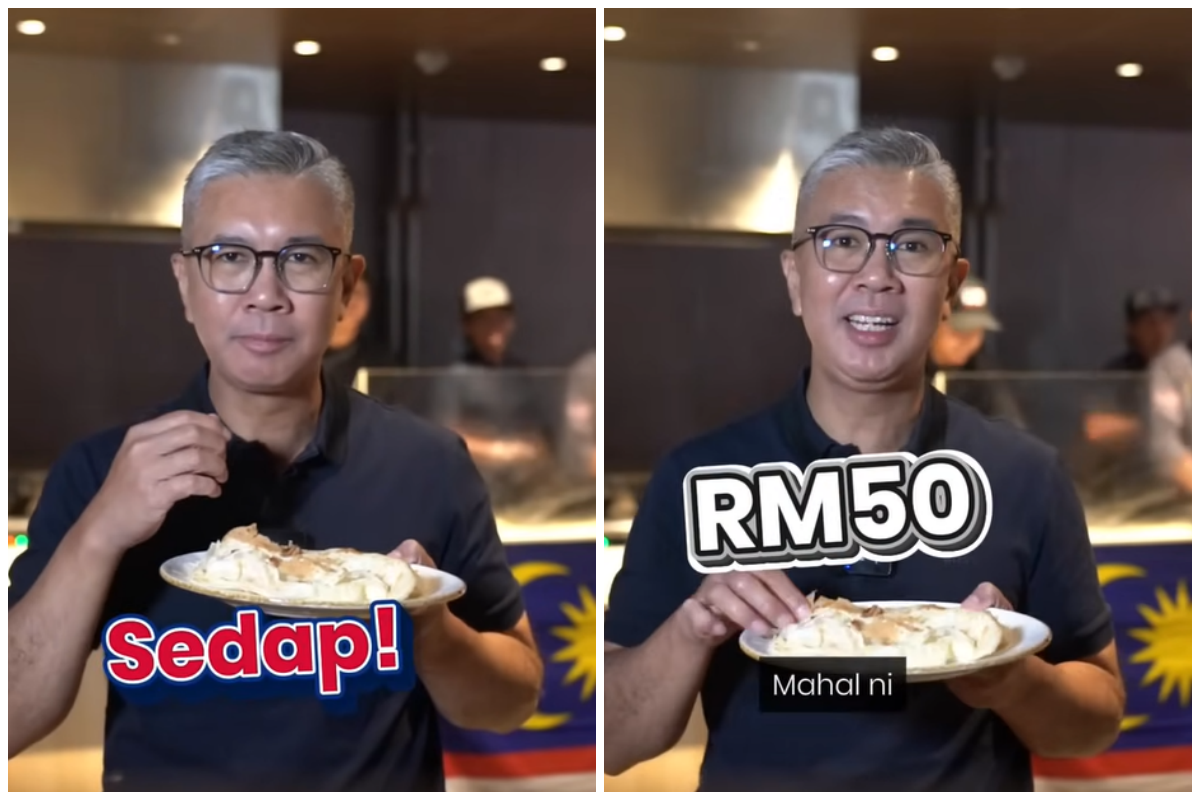

RM50 for 1 Roti Canai?! Japanese Crowd Queues 2 Hours Just to Taste ‘Flying Flatbread’

Last updated

Aug 19, 2025

“I’m merely existing” – 36yo M’sian Homeowner Can’t Afford to Turn on Aircond at Night

Last updated

Aug 19, 2025

Kid Causes RM240k Damage After Being Denied Influencer’s Labubu

Last updated

Aug 19, 2025

Fitness Enthusiast Splurges RM500k on “300-Year” Gym Membership, Owner Runs Off With Cash!

Last updated

Aug 18, 2025

Nice View, Zero Space: Malaysians Slam Viral RM650 ‘Grave Room’ in Kuala Lumpur

Last updated

Aug 18, 2025

No Winners Again! Sports Toto Jackpot Has Reached a Staggering RM77 Million

Last updated

Aug 18, 2025

Burnt Out 31yo M’sian With RM100k Savings Unsure if She Can Afford to Quit Her Toxic Job

Last updated

Aug 18, 2025

RM1,700 Minimum Wage? City Youths Still Struggling, Forced to Work 2 Jobs to Survive

Last updated

Aug 11, 2025

Software Engineer Leaves RM4k Job to Grow Chillies and Now Earns Up to RM50k per Harvest

Last updated

Aug 8, 2025

China’s Craziest Concert Promo Yet? Adopt Calves Worth RM70k and Score VIP Seats

Last updated

Aug 8, 2025

Johor Street Vendor Goes Viral After Turning Karipap Biz Into RM80K-a-Month Empire

Last updated

Aug 7, 2025

28yo Operates Waste Truck During Daytime and Drives Mercedes at Night, Internet is Shook!

Last updated

Aug 7, 2025

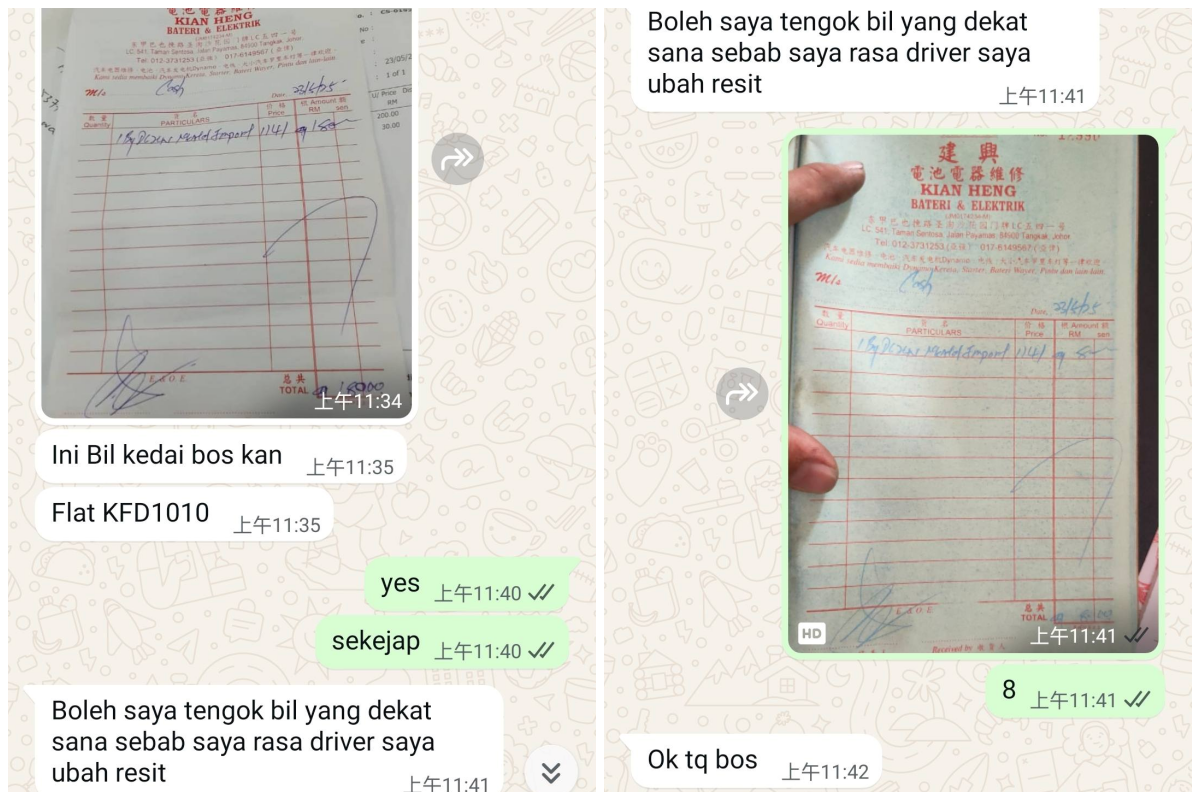

Caught in 4K: Lorry Driver Turns RM8 Light Bulb Into RM180 Claim and Gets Busted!

Last updated

Aug 6, 2025

M’sian Who Bought RM230K Bearbrick Now Can’t Sell It Even After Slashing Price by RM100K!

Last updated

Aug 6, 2025

Caught Red-Handed: SG Driver Refuels With RON95 in JB, Even Packs Extra to Go!

Last updated

Aug 5, 2025

Pickled Mango Entrepreneur Who Said He Bought a Private Jet Admits it is a Gimmick

Last updated

Jul 28, 2025

PSA: If Your MyKad’s Over 10 Years Old, It Might Be Difficult to Use the RM100 SARA Aid

Last updated

Jul 28, 2025

This Malaysian Influencer Bought a Private Jet Just by Selling Pickled Mangoes

Last updated

Jul 22, 2025

Father of 2 Who Works Away From Home Lives in His Car to Save RM1,475 on Rent

Last updated

Jul 21, 2025

Is Your RM7,000 Salary Good Enough? One Malaysian Faces Parental Pressure To Move To Singapore

Last updated

Jul 17, 2025

RM126,041 TikTok Tipping Landed Malaysian Secretary In Jail

Last updated

Jul 16, 2025

Shanghai Woman Shops So Much She Needs Another Home

Last updated

Jul 15, 2025

.png)

The Man Who Saved A Fortune By Spending Under RM4.30 Per Meal

Last updated

Jul 14, 2025

Teen Shares Her PTPTN Loan to Feed Mum & Siblings – This Family’s Story Will Break You

Last updated

Jul 9, 2025

How To File Your Taxes If You Changed Or Lost Your Job Last Year (YA 2024)

Last updated

Mar 28, 2025

9 Categories of Donations & Gifts Eligible for YA 2024 Tax Deductions

Last updated

Mar 28, 2025

Here's a List of Income Tax Relief Changes You Need to Know for YA 2024

Last updated

Mar 24, 2025

How To File Your Taxes as a Freelancer in 2025 (YA 2024)

Last updated

Mar 21, 2025

Taxpayers Can Now Repay Overdue Taxes via LHDN's New Instalment Plan

Last updated

Mar 20, 2025

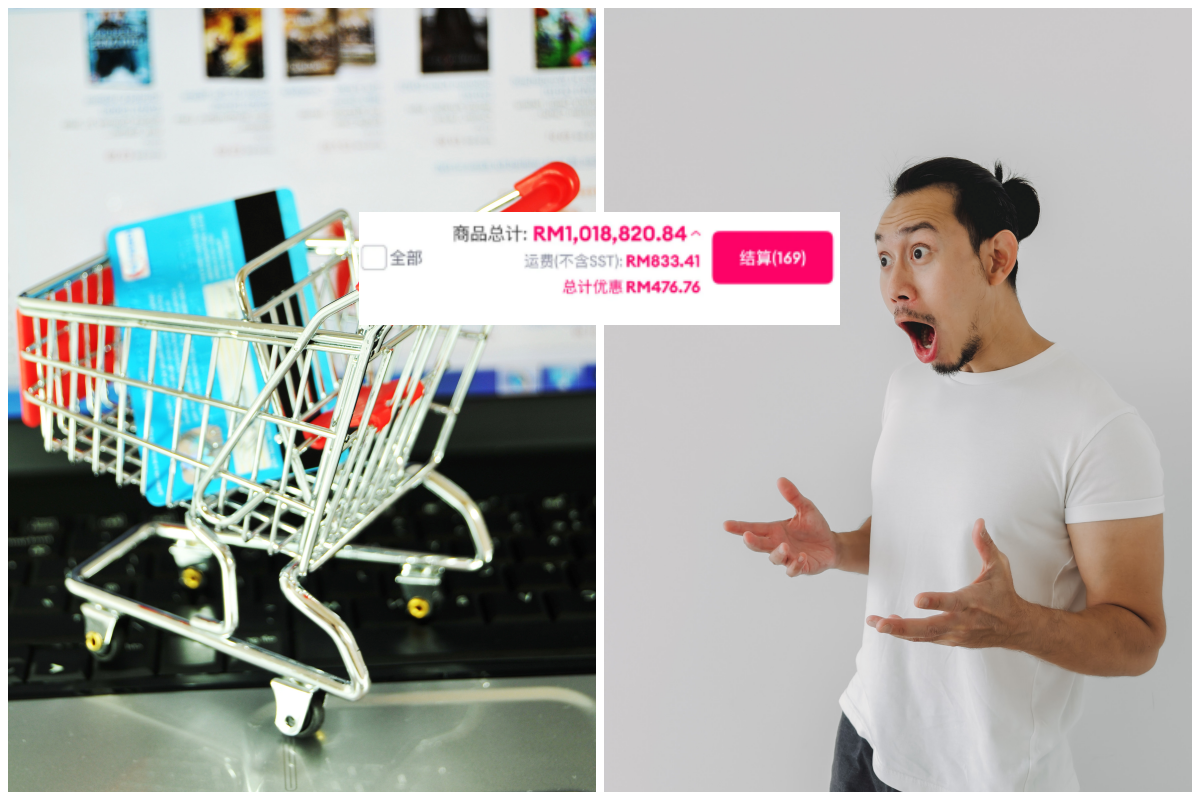

Study: M'sians Spent RM707.9 Billion or RM1,735/Mth on Online Shopping in 2024

Last updated

Mar 17, 2025

How to File Your Income Tax in 2025 (YA 2024)

Last updated

Mar 17, 2025

You Can Now Enter & Exit Parking Areas Without Tapping Your TNG Card

Last updated

Mar 14, 2025

TNG Introduces TapSecure, Feature to Replace SMS-Based One-Time Passwords

Last updated

Mar 14, 2025

5,272 Malaysians Under Age 34 Declared Bankrupt Since 2020

Last updated

Mar 13, 2025

Government & Stakeholders Unite to Tackle Rising Healthcare Costs With Long-Term Solutions

Last updated

Mar 11, 2025

Insurance & Takaful Industry are Proposing Measures to Tackle Rising Healthcare Costs

Last updated

Mar 7, 2025

Batik Air Implements Fixed Hari Raya Fares to Sabah & Sarawak

Last updated

Mar 7, 2025

Maybank has Transitioned to Secure2u for All Online Transactions Effective 6 March

Last updated

Mar 6, 2025

PMX: Malaysians Will Struggle During Retirement With Early EPF Withdrawals

Last updated

Mar 5, 2025

With High Dividend Payout, EPF Account 3 Withdrawals May Reach RM5 Billion

Last updated

Mar 4, 2025

EPF Announces Dividend of 6.30% for 2024, Highest Since 2017!

Last updated

Mar 1, 2025

Targeted Diesel Subsidies: Who is Affected?

Last updated

Jun 18, 2024

What is EPF Account 3 and How You Can Benefit

Last updated

Apr 18, 2024

PM Announces RM500 Hari Raya Cash Aid for Civil Servants

Last updated

Apr 3, 2024

What is PADU Malaysia and Why Register?

Last updated

Mar 13, 2024

EPF Announces Dividend Release for 2023: What You Need to Know

Last updated

Feb 29, 2024

What is EPF Voluntary Contribution and How Does it Work?

Last updated

Jan 16, 2024

Tax Reliefs and Exemptions You Can Enjoy in 2024

Last updated

Dec 14, 2023

.png)

Lazy Person's Guide to Achieving Financial Freedom with Minimal Effort

Last updated

Sep 7, 2023

.png)

Grow Your Wealth With The Right Banking Account

Last updated

Apr 27, 2023

How To File Your Income Tax In 2023

Last updated

Mar 16, 2023

2022 Personal Income Tax Relief (YA2022)

Last updated

Mar 3, 2023

Deposit Money On Li Chun 2023 According To Your Zodiac Sign

Last updated

Jan 27, 2023

5 Steps To Build An Emergency Fund

Last updated

Jan 12, 2023

Open An HSBC Basic Savings Account & Get RM100!

Last updated

Jan 12, 2023

5 New Year Financial Resolutions To Help You Get Richer In 2023

Last updated

Dec 21, 2022

.png)

4 Ways To Recognize Money Scams!

Last updated

Dec 21, 2022

5 Ways To Avoid A Christmas Financial Hangover

Last updated

Dec 21, 2022

4 Ways To Spring Clean Your Finances

Last updated

Dec 21, 2022

Start Saving With HSBC & Win A Dyson Pure Cool Purifier!

Last updated

Nov 17, 2022

The Do’s And Don'ts Of Currency Exchange For Your Next Vacation

Last updated

Nov 1, 2022

Try These 10 Tips To Save Money On Groceries

Last updated

Oct 28, 2022

9 Spooky Money Nightmares Every M’sian Can Relate!

Last updated

Oct 27, 2022

How Much Do M’sians Spend On Deepavali? We Asked Our Colleagues!

Last updated

Oct 21, 2022

What Does Your Fav Deepavali Food Say About Your Money Traits?

Last updated

Oct 19, 2022

6 Ways To Pay Off Your Credit Card Debt

Last updated

Oct 5, 2022

4 Financial Lessons You Can Learn From Netflix’s Get Smart With Money

Last updated

Sep 20, 2022

Understanding Your Money Personality. Which One Are You?

Last updated

Sep 14, 2022

Pay4U Makes It Possible To Clear Mortgages & Car Loans With A Credit Card

Last updated

Sep 1, 2022

.png)

Financial Privileges Malaysians Get To Enjoy!

Last updated

Aug 16, 2022

.png)

5 Habits To Help You Achieve Financial Freedom ASAP

Last updated

Aug 10, 2022

.png)

Arigato Your Money - The Japanese Secret To A Wealthier You

Last updated

Jul 29, 2022

6 Things You Should Start Doing To Cope With Rising Inflation

Last updated

Jul 6, 2022

3 Fun Money-Saving Challenges For Your Kids

Last updated

Jul 4, 2022

What happens to our debts when we die?

Last updated

Jul 1, 2022

How Much Does It Cost To Have A Wedding In M’sia?

Last updated

Jun 29, 2022

Real couples tell us financial questions to ask your future spouse

Last updated

Jun 24, 2022

My Journey To Financial Freedom Started By Investing At 19 Years Old

Last updated

Jun 22, 2022

How To Decide If You Should Rent Or Buy A House?

Last updated

Jun 20, 2022

Celebrate World Cup 2022 with Bank Islam’s Limited Edition Visa FIFA-Themed Credit Card-i

Last updated

Jun 15, 2022

5 self-care activities you can do in Klang Valley with RM100

Last updated

Jun 14, 2022

4 Ways To Keep Your Family Financially Protected After Your Death

Last updated

Jun 7, 2022

Everything You Need To Know About Your Monthly Payslip

Last updated

May 30, 2022

Avoid These 5 Bad Payday Habits If You're Broke All The Time

Last updated

May 24, 2022

Driving vs Grab: Which is more cost-effective?

Last updated

May 17, 2022

When is it okay to utilise EPF’s Special Withdrawal facility?

Last updated

Apr 5, 2022

A Step-to-Step Guide for the Special RM10,000 EPF Withdrawal

Last updated

Apr 1, 2022

T20, M40 And B40 Income Classifications In Malaysia

Last updated

Mar 24, 2022

5 Ways To Improve Your Credit Score

Last updated

Mar 22, 2022

How To File Your Income Tax In 2022

Last updated

Mar 16, 2022

4 Ways A Bad Credit Score Can Impact Your Life (And How You Can Fix That)

Last updated

Mar 15, 2022

Income Tax Malaysia 2022: Who Pays and How Much?

Last updated

Mar 10, 2022

Ultimate Guide To Credit Scores

Last updated

Mar 8, 2022

Malaysia Personal Income Tax E-filling Guide (2021 LHDN)

Last updated

Mar 7, 2022

How Malaysians Can Check Their Credit Score For FREE Via CompareHero.my

Last updated

Mar 4, 2022

#DearGenZ: Here Are 7 Money Mistakes You Can Learn From Millennials (And Never Repeat)

Last updated

Mar 1, 2022

#NewNormal: How Your Business Can Survive The COVID-19 Pandemic

Last updated

Mar 1, 2022

10 Examples of Poor Money Management (& What You Can Do About It)

Last updated

Mar 1, 2022

15 Financial Mistakes to Avoid in 2019

Last updated

Mar 1, 2022

4 Benefits You Can Get If You Save Your EPF Money

Last updated

Mar 1, 2022

5 Reasons Not To Lend Money To Your Friends

Last updated

Mar 1, 2022

5 Ways To Make Extra Money By Renting Out Unused Space

Last updated

Mar 1, 2022

6 Ways to Lower Your Electricity Bill

Last updated

Mar 1, 2022

6 Ways To Stop Impulse Shopping

Last updated

Mar 1, 2022

7 Important Costs You Might Not Be Budgeting For

Last updated

Mar 1, 2022

8 Places You Can Get Cheap Grocery Delivery in Malaysia

Last updated

Mar 1, 2022

Everything You Need To Know About Emergency Fund

Last updated

Mar 1, 2022

How Much Money Should You Give Back To Your Parents?

Last updated

Mar 1, 2022

How To Make A Budget Calendar That Will Work For You

Last updated

Mar 1, 2022

Know Your Rights As A Consumer of Prepaid Services in Malaysia

Last updated

Mar 1, 2022

Mild Inflation In 2022: But What Is It And How Can You Cope With Inflation?

Last updated

Mar 1, 2022

Money Management Tips by Mooi Li, Juice Works Founder [Exclusive]

Last updated

Mar 1, 2022

Money Talk with Ili Sulaiman, Co-Founder of Agak Agak

Last updated

Mar 1, 2022

Top Lazada And Shopee Tips And Tricks Every Online Shopper Must Know!

Last updated

Mar 1, 2022

What Is the 30-Day Rule in Saving Money, And How Does It Control Impulse Buying?

Last updated

Mar 1, 2022

#CNY2021 - Shopee & Lazada CNY Sale: 27 Last-Minute Gift Ideas For Your Family And Friends

Last updated

Mar 1, 2022

#StretchYourRinggit - How To Survive A Pay Cut During COVID-19

Last updated

Mar 1, 2022

Here's How To Know If You Have Unclaimed Money Kept By The Government

Last updated

Mar 1, 2022

Swap your cigarettes out for a car - can ah?

Last updated

Mar 1, 2022

10 Personal Finance Instagram Accounts You Should Follow

Last updated

Mar 1, 2022

10 Smart Ways You Can Spend RM1,000 Right Now

Last updated

Mar 1, 2022

10 Tips To Save RM800 A Month

Last updated

Mar 1, 2022

11 Expenses You Must Know Before Owning A Cat In Malaysia

Last updated

Mar 1, 2022

11 Practical Hacks To Reduce Your Financial Burden And Stress

Last updated

Mar 1, 2022

4 Practical Ways To Afford Groceries In Malaysia

Last updated

Mar 1, 2022

5 Important Questions To Ask When You Interview A Financial Planner Or Advisor

Last updated

Mar 1, 2022

5 Polite Ways To Ask For Your Money Back

Last updated

Mar 1, 2022

5 Real-Life Financial Lessons From Movies And TV Shows

Last updated

Mar 1, 2022

5 Stages Of Financial Independence

Last updated

Mar 1, 2022

5 Supermarket Store Brand Items That Can Save You Money

Last updated

Mar 1, 2022

5 Tips To Stop Living Pay Cheque To Pay Cheque

Last updated

Mar 1, 2022

5 Ways To Control Your Family Budget

Last updated

Mar 1, 2022

6 Money Myths We Need To Stop Believing

Last updated

Mar 1, 2022

6 Ways To Save On Air Conditioning Costs In Malaysia

Last updated

Mar 1, 2022

6 Ways To Reduce Your Entertainment Expenses

Last updated

Mar 1, 2022

6 Ways To Set Yourself Up For Financial Freedom In Your 20s

Last updated

Mar 1, 2022

8 Financial Planning Tips For Malaysian Gen Zs

Last updated

Mar 1, 2022

Bantuan Prihatin Nasional 2.0: Here’s What You Need To Know

Last updated

Mar 1, 2022

Comparing Loyalty Cards to Get the Most Rewards

Last updated

Mar 1, 2022

Everything You Need To Know About Zakat In Malaysia

Last updated

Mar 1, 2022

Financial Literacy Web Game Mind Your Ringgit Aims To Educate Young Malaysians

Last updated

Mar 1, 2022

Financial Tips You Should Know For 2016

Last updated

Mar 1, 2022

How Much Will A Divorce Procedure Cost You in Malaysia?

Last updated

Mar 1, 2022

How to Cut Down Expenses While Living in a Big City

Last updated

Mar 1, 2022

How To Recession-Proof Your Finances

Last updated

Mar 1, 2022

How To Safeguard Your Rights As A Consumer In Malaysia

Last updated

Mar 1, 2022

KCLau, Mr Stingy and RinggitOhRinggit Share Their Resolutions and Top Tips for 2017

Last updated

Mar 1, 2022

Mr Stingy: Tips on Leading a Successful Life For Millennials

Last updated

Mar 1, 2022

Save Money By Making Your Own RM5 Meals

Last updated

Mar 1, 2022

The Best Personal Finance Books For Beginners

Last updated

Mar 1, 2022

Top 5 Personal Finance Podcasts in Malaysia

Last updated

Mar 1, 2022

Use These 7 Cash Tricks to Grow Your Savings

Last updated

Mar 1, 2022

We Asked Malaysian Bloggers For Financial Management Tips For Couples!

Last updated

Mar 1, 2022

Why Keeping Your Finances A Secret Is Bad For Your Relationship

Last updated

Mar 1, 2022

You Can Save Money by Not Wasting Food, Here’s How

Last updated

Mar 1, 2022

4 Interesting Facts You Didn't Know About The Malaysian Ringgit

Last updated

Mar 1, 2022

How To Kick-Start Your Child's Life Savings

Last updated

Mar 1, 2022

100 Ideas for Personal Finance

Last updated

Feb 21, 2022

11 Tips To Simplify Your Financial Life

Last updated

Feb 21, 2022

Budget 2022: Here Are The Key Highlights And Takeaways For You

Last updated

Feb 21, 2022

Here Are The Tax Reliefs & Exemptions You Can Enjoy in 2022

Last updated

Feb 21, 2022

Pre-Merdeka vs 2022: How Malaysians Managed Their Money Then vs Now

Last updated

Feb 21, 2022

Planning Your Investments For 2022? Here's What You Should Keep In Mind

Last updated

Feb 21, 2022

5 Bad Financial Advice that Makes You Poorer

Last updated

Feb 21, 2022

5 Extensions That Can Help You Save While Shopping Online

Last updated

Feb 21, 2022

Money Lessons From 2021 That Can Help You Save More In 2022

Last updated

Feb 21, 2022

Public Holidays in Malaysia & Long Weekends You Can Enjoy in 2022

Last updated

Feb 21, 2022

We Asked 5 People What Their New Year Resolutions Are In 2022. Here’s What They Said

Last updated

Feb 21, 2022

What Are Investments And How To Start It

Last updated

Feb 21, 2022

Want To Help #MalaysiaBanjir Victims? Here's What You Can Do

Last updated

Feb 21, 2022

Want Some Extra Cash? Here Are 5 Free Apps You Can Earn Money From

Last updated

Feb 18, 2022

How To Get Your Money Back From Financial Scams

Last updated

Feb 11, 2022

6 Ways To Sell Your Unwanted Stuff For Money

Last updated

Feb 10, 2022

Budget 2022: Analysing The Measures Through A Personal Finance Lense

Last updated

Feb 9, 2022

Budget 2022: What's In It For The Real Estate Sector and Property Buyers?

Last updated

Feb 9, 2022

Income Tax For Foreigners Working in Malaysia 2022

Last updated

Feb 9, 2022

Income Tax Relief: What Can You Claim In 2022 For YA 2021?

Last updated

Feb 9, 2022

How do I calculate my Debt Service Ratio?

Last updated

Dec 28, 2021

Tabung Harapan Malaysia: Hope Fund For Malaysia By Malaysians

Last updated

Dec 28, 2021

What Actually Happens When You Go To AKPK For Help?

Last updated

Dec 22, 2021

Guide to Calculating Flat Rate Interest and Reducing Balance Rate

Last updated

Dec 7, 2021

Online Scams in Malaysia You Need To Know About

Last updated

Nov 23, 2021

Budget 2022: 5 Key Highlights And What You Get From Them

Last updated

Nov 1, 2021

You Can Have 4 Types of Bank Accounts in Malaysia, But What's Right For You?

Last updated

Oct 4, 2021

3 Ways You Can Settle Your Debts In Malaysia

Last updated

Sep 10, 2021

Transferred Money To The Wrong Bank Account? Here's What You Should Do

Last updated

Sep 6, 2021

Are You Eligible For The Special Covid-19 Assistance (BKC)? Here's How You Can Find Out

Last updated

Sep 2, 2021

6 Things To Know About The Moratorium Before You Sign Up For It

Last updated

Jul 10, 2021

Should You Open A Joint Bank Account With Your Spouse?

Last updated

Jun 30, 2021

Highlights on PM Muhyiddin's RM150 Bil Pemulih Aid Package

Last updated

Jun 29, 2021

Budget 2020 / Belanjawan 2020 Needs Your Ideas And Suggestions

Last updated

Jun 28, 2021

3 Easy Ways For Maybank Customers To Apply For COVID-19 Post-Moratorium Assistance

Last updated

Jun 25, 2021

4 Reasons Why Your Business Should Have a Business Bank Account

Last updated

Jun 8, 2021

Personal Banking vs Business Banking: Do I Need Separate Accounts?

Last updated

Jun 8, 2021

Budget 2020: Live Updates On Oct 11

Last updated

Jun 1, 2021

7 Common Things Malaysians Don’t Realise Are A Waste Of Money

Last updated

Apr 28, 2021

Know The Difference Between Good Debt and Bad Debt

Last updated

Apr 28, 2021

How Do You Survive From Bankruptcy?

Last updated

Apr 27, 2021

Comparing SST VS GST: What's The Difference?

Last updated

Apr 23, 2021

How Bank Interest Rates Work On A Savings Account? Here’s A Mini Guide

Last updated

Apr 23, 2021

What's The Penalty For Filing Your Income Tax Late?

Last updated

Apr 12, 2021

6 Ways You Can Pay Less Income Tax In Malaysia

Last updated

Apr 8, 2021

Tax Relief vs Tax Rebate: What's The Difference?

Last updated

Apr 6, 2021

Job Loss Amid CMCO: How To Bounce Back From Retrenchment

Last updated

Mar 22, 2021

Bajet 101: Langkah Menyediakan Penyata Pendapatan Peribadi

Last updated

Mar 9, 2021

What To Do When Debt Collection Agency Knocks On Your Door

Last updated

Mar 9, 2021

What You Need To Know About Bankruptcy In Malaysia

Last updated

Feb 10, 2021

8 Money Tips For Chinese New Year

Last updated

Feb 8, 2021

8 Ways To Make Your Angpow Money Work For You

Last updated

Feb 5, 2021

I’m Only 21 Years Old. Do I Need A Credit Score?

Last updated

Feb 5, 2021

Ask The Expert: Avoid These 6 Mistakes If You Want A Great Credit Score

Last updated

Jan 29, 2021

BNM Maintains OPR At 1.75% - What Does This Mean For Malaysians?

Last updated

Jan 27, 2021

Don’t Fall For These 5 Credit Score Myths!

Last updated

Jan 18, 2021

#CHInsights - How Does Credit Accessibility Impact Financial Inclusivity?

Last updated

Jan 14, 2021

Online Love Scams: Here’s How To Outsmart A Romance Scammer!

Last updated

Jan 4, 2021

Best 12.12 Credit Card Discounts For Shopee

Last updated

Dec 11, 2020

Best 12.12 Deals On Lazada For Secret Santa

Last updated

Dec 11, 2020

#DigitalCareers: How To File Your Income Tax As A Freelancer

Last updated

Dec 3, 2020

Bank Negara Malaysia Reassures Borrowers Repayment Assistance To Continue Until Next Year

Last updated

Nov 27, 2020

How To Read Your Credit Report Using This Code

Last updated

Nov 25, 2020

BNM Announces Additional Measures To Assist Individuals And SMEs Affected By COVID-19

Last updated

Nov 11, 2020

Is Your Credit Score Good Enough To Get You A Mortgage? Here’s Why It Matters

Last updated

Nov 5, 2020

How Malaysians Can Take Advantage Of The Lower Overnight Policy Rate (OPR)

Last updated

Nov 4, 2020

Banking Institutions To Assist Borrowers And Customers In CMCO And EMCO Areas

Last updated

Oct 13, 2020

All You Need To Know About Maybank’s New MAE Mobile Banking App And MAE Visa Debit Card

Last updated

Oct 12, 2020

Maybank - First Bank To Introduce Online Appointment Management System, EzyQ

Last updated

Oct 9, 2020

5 Things To Do Now That You’ve Got A Side Income In Malaysia

Last updated

Sep 10, 2020

7 Types Of Shocking COVID-19 Scams All Malaysians Need To Be Aware Of

Last updated

Sep 10, 2020

How To Apply For 6 Malaysian Government Welfare Benefits & Social Assistance

Last updated

Sep 10, 2020

Digital Banks Are On the Rise In Malaysia - What Does This Mean for You? Experts Weigh In

Last updated

Aug 27, 2020

What Is A CTOS & CCRIS Report And What's Their Difference?

Last updated

Aug 18, 2020

From Zero To Hero: 5 Financial Lessons From Liverpool FC Everyone Can Learn From

Last updated

Jul 10, 2020

10 Simple Ways To Avoid Getting Scammed (And What To Do If You’re A Victim)

Last updated

Jul 8, 2020

What Happens If You Can't Pay Your Loans In Malaysia Post-MCO (And How To Fix This Fast)

Last updated

Jul 1, 2020

#NewNormal: 7 Tips To Buy A House In Malaysia During COVID-19 Pandemic

Last updated

Jun 23, 2020

#NewNormal: Should You Buy A New Property After COVID-19? Here’s What The Experts Say

Last updated

Jun 17, 2020

#StretchYourRinggit: 9 Brands With Rewarding Recycling Programs In Malaysia

Last updated

Jun 17, 2020

12 Easy Ways To Protect The Environment While Saving Money

Last updated

Jun 11, 2020

How To Increase Your Credit Limit Without Affecting Your Credit Score In Malaysia

Last updated

Jun 11, 2020

7 Strategies To Get Out Of Debt Fast During The COVID-19 Pandemic

Last updated

Jun 4, 2020

2020 OPR Cuts: What Does This Mean For Malaysians? [UPDATED]

Last updated

Feb 9, 2020

The Best 2020 Ang Pao Guide: Who To Give & How Much?

Last updated

Jan 21, 2020

Budget 2019: Summary Infographics To See

Last updated

Jan 16, 2020

7 School Holiday Activity Ideas

Last updated

Jan 16, 2020

9 Digital Mobile Payments in Malaysia That You Need To Know About

Last updated

Jan 16, 2020

Maybank: Service Charge for Card & Loan Repayments begin 1 October 2019

Last updated

Jan 16, 2020

It's Good To Be A Selangorian!

Last updated

Jan 16, 2020

How Much Do You Know About Islamic Finance?

Last updated

Jan 15, 2020

Highlight of Consumer Credit Law at National Strategy for Financial Literacy Launch

Last updated

Nov 25, 2019

Citibank Application is Now 100% Online - What Does This Mean?

Last updated

Nov 25, 2019

CompareHero's parent, CompareAsiaGroup raises US$20M in Series B1 funding led by Experian

Last updated

Nov 25, 2019

Is RM500 Enough To Encourage Women To Start Working Again?

Last updated

Nov 20, 2019

Budget 101: How to Create a Personal Cash Flow Statement

Last updated

Nov 19, 2019

Pennywise, Not So Pound Foolish

Last updated

Nov 19, 2019

Here Are The Best Cash Financing Options

Last updated

Nov 19, 2019

Budget 2016 Revised: What You Need To Know

Last updated

Oct 31, 2019

5 Things You Should Know Now about Budget 2016

Last updated

Oct 31, 2019

Budget 2014: A Difficult Act for Government

Last updated

Oct 31, 2019

Everything You Need To Know About BR1M 2016

Last updated

Oct 31, 2019

Which Is The Best Digital Wallet: Visa Checkout, PayPal or MasterPass?

Last updated

Oct 31, 2019

RHB Launches Multi-Currency Debit Card Supporting 13 Foreign Currencies

Last updated

Oct 22, 2019

Malaysia Budget 2019 - Live Updates at 4PM

Last updated

Oct 10, 2019

Budget 2020: What Can We Expect?

Last updated

Oct 8, 2019

Don't Let The Haze Cloud Your Spending Judgment

Last updated

Oct 2, 2019

The MVPs of Malaysian Football

Last updated

Sep 26, 2019

Are You Financially Better Or Worse Than Average Malaysian? [INFOGRAPHIC]

Last updated

Sep 12, 2019

New Taxation Rates In Malaysia According To Budget 2019

Last updated

Sep 3, 2019

How Serious Is Malaysia's RM1 Trillion Debt?

Last updated

Sep 3, 2019

7 REAL Crazy Rich Kids of Asia

Last updated

Aug 28, 2019

Money Lessons I Learned From My Dad

Last updated

Aug 27, 2019

Here's 6 Ways To Spend Your Duit Raya

Last updated

Aug 27, 2019

6 Ways You Are Wasting Money

Last updated

Aug 27, 2019

CIMB, OCBC, & RHB Reduces Their Base Rates & Base Lending Rates

Last updated

Aug 27, 2019

Don’t shop at Mid Valley & The Gardens Mall – not without this.

Last updated

Aug 27, 2019

National Strategy for Financial Literacy 2019-2023

Last updated

Aug 26, 2019

Chinese New Year Ang Pow – What does it mean?

Last updated

Aug 23, 2019

Don’t Become a Victim of Work-from-Home Scams

Last updated

Aug 23, 2019

The #30DaysBudgetHero Challenge: Completing Ramadhan on RM1,000

Last updated

Aug 23, 2019

Understanding Living Wage in Malaysia

Last updated

Aug 23, 2019

What Is Missing From Budget 2018? Here Are What The Experts Think

Last updated

Aug 23, 2019

UnionPay - The Leading Global Payment Network

Last updated

Aug 23, 2019

Impact Of Income Gap and Disparity of Wealth In Malaysia

Last updated

Aug 19, 2019

Overdraft Facilities: A Type Of Demand Loan Offered By Banks

Last updated

Aug 19, 2019

How To Sign Up & Use Alipay Mobile Wallet In Malaysia

Last updated

Aug 5, 2019

Types Of Money & Investment Scams You Often See In Malaysia

Last updated

Aug 5, 2019

7 Tax Exemptions in Malaysia You Should Know About

Last updated

Jul 26, 2019

Survey: How much did you spend this Raya?

Last updated

Jun 7, 2019

To Malaysians, From Malaysians: Do Better For Your Retirement

Last updated

May 27, 2019

BelanjawanKu - A Guide For A Better Budget

Last updated

May 27, 2019

How To Share Expenses Fairly As A Couple [INFOGRAPHIC]

Last updated

May 3, 2019

What Is Your Net Worth?

Last updated

May 3, 2019

Money Lessons You Can Learn From Game Of Thrones

Last updated

Apr 22, 2019

Money Management: 3 Ways to Control Your Finances

Last updated

Apr 19, 2019

Budget 2014: What’s in it for the Malaysian youth?

Last updated

Apr 15, 2019

6% Tax on Digital Services passed, begins 1 Jan 2020

Last updated

Apr 9, 2019

In support of International Women's day: Malaysia's 25 Richest Women

Last updated

Apr 9, 2019

Find Out What These Credit Reporting Agencies Say About Your Credit History

Last updated

Apr 8, 2019

Resolve Your Financial Complaints For Free With The Financial Mediation Bureau!

Last updated

Apr 3, 2019

Don't Fall For MLM Scams, Listen to Our Interview With BFM Radio [PODCAST]

Last updated

Apr 3, 2019

All You Need To Know For 2016 Income Tax Filing [INFOGRAPHIC]

Last updated

Apr 2, 2019

Everything You Need to Know About Filing Your Income Tax [INFOGRAPHIC]

Last updated

Apr 2, 2019

Outstanding Income Tax Refunds in the past years? Get it back in 2018 – LGE

Last updated

Apr 2, 2019

The Complete Malaysia Personal Income Tax Guide 2018 (YA 2017) [INFOGRAPHIC]

Last updated

Apr 2, 2019

[2017 Tax Planning] Start to record these early, Don't wait until year end

Last updated

Apr 2, 2019

Bitcoin Debit Cards: An Introduction to Malaysians

Last updated

Apr 1, 2019

Interest Rates: Nominal meets Real meets Effective

Last updated

Apr 1, 2019

The AmBank Group/RHB Banking Group Merger: How will it affect you?

Last updated

Apr 1, 2019

Budget 2019 Malaysia: Looking at the Rakyat's Suggestions

Last updated

Apr 1, 2019

Budget 2019 Malaysia: Revisiting Budget 2018 Malaysia

Last updated

Apr 1, 2019

Common Money Mistakes People Made in 2018

Last updated

Apr 1, 2019

Price Controlled Items This Deepavali

Last updated

Apr 1, 2019

How You Duit? (Blogger Edition!)

Last updated

Mar 31, 2019

Malaysia’s Personal Finance Roundup 2018

Last updated

Mar 27, 2019

The Economic Outlook and Drivers of Growth in Malaysia

Last updated

Mar 27, 2019

The B40 Budget - Fair and Just?

Last updated

Mar 27, 2019

Budget 101: How to Make a Personal Income Statement

Last updated

Mar 27, 2019

How You Duit - Blogger Edition 2

Last updated

Mar 22, 2019

Budget 101: How to Create a Personal Balance Sheet

Last updated

Mar 21, 2019

Malaysians Share Their True Feelings about Budget 2017

Last updated

Mar 13, 2019

The Basic of Islamic Banking

Last updated

Mar 11, 2019

Bajet 2018: Will the Rakyat Get What They Want?

Last updated

Mar 11, 2019

Samsung Pay in Malaysia: Here’s What You Need to Know

Last updated

Mar 11, 2019

The Cost of Living Battle: Kuala Lumpur Vs. Johor

Last updated

Mar 11, 2019

The Cost of Living Battle: Kuala Lumpur Vs. Penang

Last updated

Mar 11, 2019

Top 10 Richest Women in Malaysia 2019

Last updated

Mar 8, 2019

Transferring Money to the UK? Here’s a Cheaper Way

Last updated

Mar 4, 2019

Differences Between Syariah and Conventional Financing

Last updated

Mar 4, 2019

Get Red-Carpet Treatment with Premier Banking Privileges

Last updated

Mar 4, 2019

How to Save up to RM6000 on Taxes This Year

Last updated

Mar 4, 2019

Key Highlights Of Malaysia Budget 2016 [INFOGRAPHIC]

Last updated

Mar 1, 2019

Key Updates: Budget 2017 Malaysia

Last updated

Mar 1, 2019

Some citi folk wants you to be FREE with our next giveaway

Last updated

Sep 29, 2018

Budget 2017: What do the experts say?

Last updated

Oct 27, 2016

Our Mission

We'll help you make your next financial move the right one.